Why Now Is Still a Great Time To Sell Your House

If you were worried buyer demand disappeared when mortgage rates went up, the data shows there are plenty of interested buyers still out there. The housing market isn't as frenzied as it was during the ‘unicorn’ years when buyer demand was through the roof, mortgage rates were historically low, and

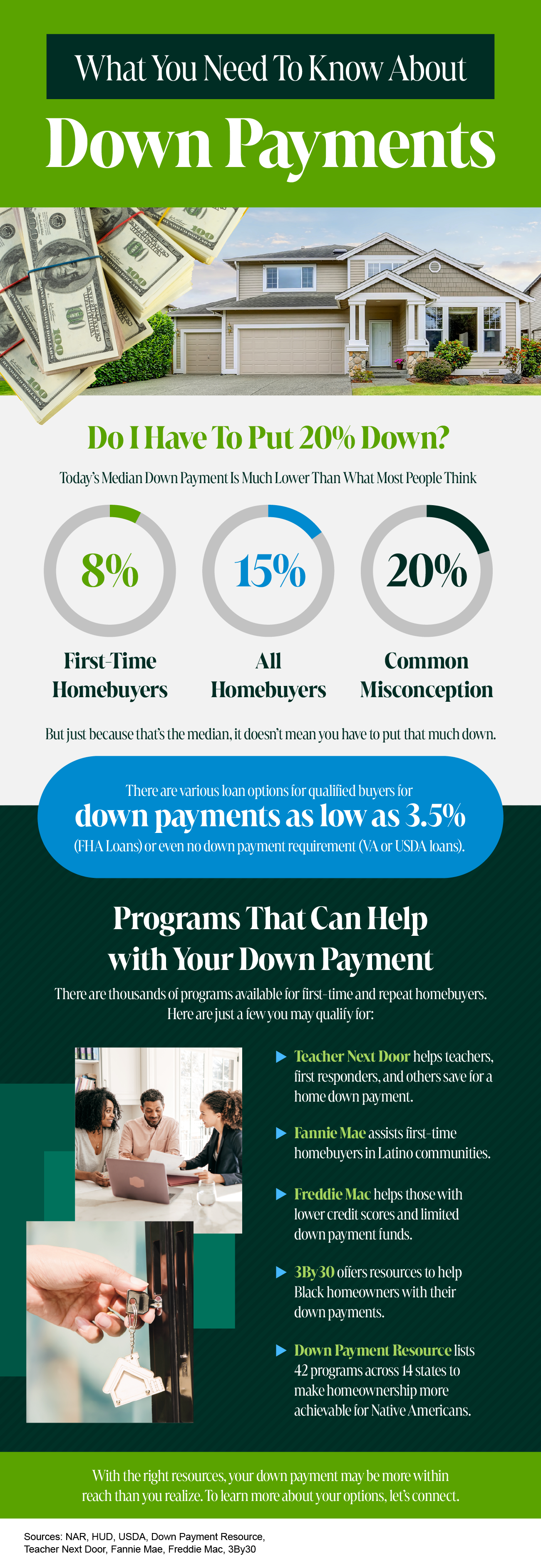

Read MoreWhat You Need To Know About Down Payments

If Your House Hasn’t Sold Yet, It May Be Overpriced

Has your house been sitting on the market a while without selling? If so, you should know that’s pretty unusual, especially right now. That’s because the supply of homes available for sale is still far lower than what we’d see in a normal year. That means buyers have fewer options than they usually

Read MoreThe Surprising Trend in the Number of Homes Coming onto the Market

If you're thinking about moving, it's important to know what's happening in the housing market. Here's an update on the supply of homes currently for sale. Whether you're buying or selling, the number of homes in your area is something you should pay attention to. In the housing market, there are re

Read MoreDown Payment Assistance Programs Can Help Pave the Way to Homeownership

If you’re looking to buy a home, your down payment doesn’t have to be a big hurdle. According to the National Association of Realtors (NAR), 38% of first-time homebuyers find saving for a down payment the most challenging step. But the reality is, you probably don’t need to put down as much as you t

Read MoreThe Perfect Home Could Be the One You Perfect After Buying

There’s no denying mortgage rates and home prices are higher now than they were last year and that’s impacting what you can afford. At the same time, there are still fewer homes available for sale than the norm. These are two of the biggest hurdles buyers are facing today. But there are ways to over

Read More-

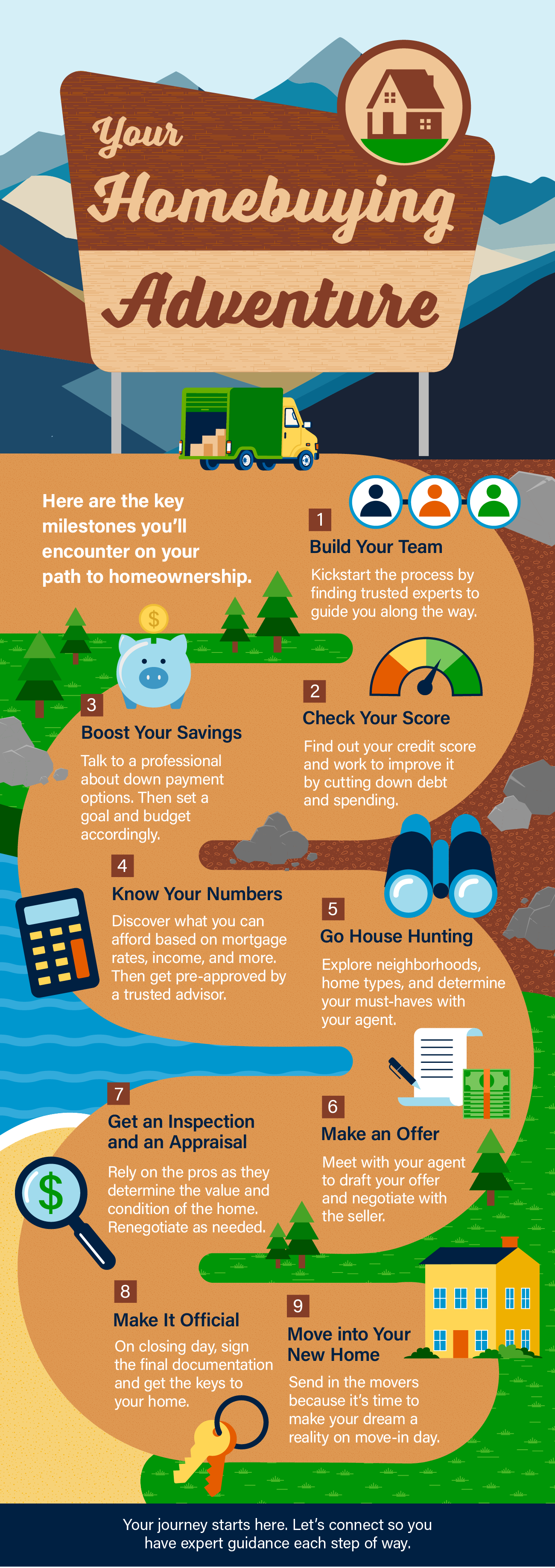

Why You Need To Use a Real Estate Agent When You Buy a Home

If you’ve recently decided you’re ready to become a homeowner, chances are you’re trying to figure out what to do first. It can feel a bit overwhelming to know where to start, but the good news is you don’t have to navigate all of that alone. When it comes to buying a home, there are a lot of moving

Read MoreHow To Turn Homeownership into a Side Hustle

Does the rising cost of just about everything these days make your dream of owning your own home feel less within reach? According to Bankrate, many people are seeking additional income through side hustles, possibly to cope with those increasing expenses and save for a home. This trend is particula

Read MoreWhen You Sell Your House, Where Do You Plan To Go?

If you’re thinking about selling your house, you may have heard the supply of homes for sale is still low, and that means your house should stand out to buyers who are craving more options. But you may also be wondering, once you sell, how does the current supply impact your own move? And, will you

Read MoreExperts Project Home Prices Will Rise over the Next 5 Years

Even with so much data showing home prices are actually rising in most of the country, there are still a lot of people who worry there will be another price crash in the immediate future. In fact, a recent survey from Fannie Mae shows that 23% of consumers think prices will fall over the next 12 mon

Read More3 Reasons To Sell Your House Before the New Year

Is Owning a Home Still the American Dream for Younger Buyers?

Everyone has their own idea of the American Dream, and it's different for each person. But, in a recent survey by Bankrate, people were asked about the achievements they believe represent the American Dream the most. The answers show that owning a home still claims the #1 spot for many Americans tod

Read MoreWhy the Economy Won’t Tank the Housing Market

If you’re worried about a coming recession, you’re not alone. Over the past couple of years, there’s been a lot of recession talk. And many people worry, if we do have one, it would cause the unemployment rate to skyrocket. Some even fear that a spike in unemployment would lead to a rash of foreclos

Read MoreAre the Top 3 Housing Market Questions on Your Mind?

When it comes to what’s happening in the housing market, there’s a lot of confusion going around right now. You may hear one thing in conversation with your friends, see something totally different on the news, and read something on social media that contradicts both of those thoughts. And, if you’r

Read MoreIs Wall Street Buying Up All the Homes in America?

If you’re thinking about buying a home, you may find yourself interested in the latest real estate headlines so you can have a pulse on all of the things that could impact your decision. If that’s the case, you’ve probably heard mention of investors, and wondered how they’re impacting the housing ma

Read MoreWhy Homeowners Are Thankful They Own

Countless people have set out on the exciting journey of homeownership. Ask around and you’ll find the vast majority are thankful they took the leap and bought a home. But why? It’s because of the many emotional and lifestyle benefits that come with being a homeowner. So, if you’re trying to decide

Read MoreHome Prices Still Growing – Just at a More Normal Pace

If you’re feeling a bit muddy on what’s happening with home prices, that’s no surprise. Some people are still saying prices are falling, even though data proves otherwise. Part of that misconception is because people are getting their information from unreliable sources. But it’s also coming from so

Read MoreAre There Actually More Homes for Sale Right Now?

If you’re looking to make a move, you want to be sure you have the latest information on the housing market. To help make that possible, here’s an update on the supply of homes for sale today. Whether you’re looking to buy or sell, the number of homes available in your local market matters to you. T

Read MoreIs Your House the Top Thing on a Buyer’s Wish List this Holiday Season?

This time every year, homeowners who are planning to move have a decision to make: sell now or wait until after the holidays? Some sellers with homes already on the market may even remove their listing until the new year. But the truth is, many buyers want to purchase a home for the holidays, and yo

Read More

Categories

Recent Posts