¿Cuánto Paga el Comprador en Closing Costs en Texas? Guía 2026

Infografía explicativa sobre el desglose de closing costs y gastos de cierre para compradores de propiedades en San Antonio y Texas 2026 Categoría: Compradores / Mercado San Antonio | 12 de junio de 2026 ¿Cuánto Paga el Comprador en Closing Costs en Texas? Guía 2026 ¿Cuánto paga el comprador en cl

Read MoreExención de Homestead en Texas: Cómo Solicitarla y Ahorrar en Tus Impuestos de Propiedad

Categoría: Compradores / Mercado San Antonio | 10 de junio de 2026 Exención de Homestead en Texas: Cómo Solicitarla y Ahorrar en Tus Impuestos de Propiedad ¿Qué es la exención de homestead en Texas y cuánto puedes ahorrar? La exención de homestead reduce el valor catastral de tu residencia princip

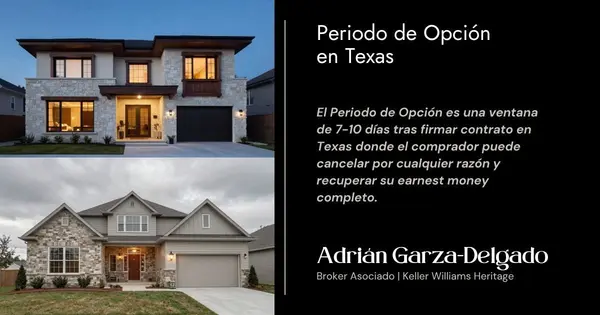

Read MoreEl Periodo de Opción en Texas: Tu Red de Seguridad al Comprar Casa

Categoría: Compradores / Mercado San Antonio | 8 de junio de 2026 El Periodo de Opción en Texas: Tu Red de Seguridad al Comprar Casa ¿Qué es el Periodo de Opción en Texas y cómo te protege? El Periodo de Opción es un número de días negociable (típicamente 7–10) después de que el contrato se firma,

Read More¿Puedes Comprar Casa en Texas Sin Ser Residente? Guía 2026 para Mexicanos y Extranjeros

Categoría: Compradores Extranjeros / Foreign National Mortgage | 29 de mayo de 2026 ¿Puedes Comprar Casa en Texas Sin Ser Residente? Guía 2026 para Mexicanos y Extranjeros ¿Puede un mexicano o extranjero comprar casa en San Antonio, Texas? Sí. Cualquier persona extranjera puede comprar una propied

Read MoreWhy a Newly Built Home Might Be the Move Right Now

Are you looking for better home prices, or even a lower mortgage rate? You might find both in one place: a newly built home. While many buyers are overlooking new construction, it could be your best opportunity in today’s market. Here’s why.There are more brand-new homes available right now than the

Read MoreMortgage Rates Are Stabilizing – How That Helps Today’s Buyers

Over the past few years, affordability has been the biggest challenge for homebuyers. Between rapidly rising home prices and higher mortgage rates, many have felt stuck between a rock and a hard place. But, something pretty encouraging is happening. While affordability is still tight, mortgage rates

Read MoreThe Advice First-Time Homebuyers Need To Hear

Buying your first home is a big milestone – and the right support is going to make it a whole lot easier. Because while this process might be brand new to you, it’s not new to your agent. They’ve helped plenty of first-time buyers through it. They know what works, what actually matters, and how you

Read MoreThe Truth About Where Home Prices Are Heading

There are plenty of headlines these days calling for a housing market crash. But the truth is, they’re not telling the full story. Here’s what’s actually happening, and what the experts project for home prices over the next 5 years. And spoiler alert – it’s not a crash. Yes, in some local markets, p

Read MoreSelling and Buying at the Same Time? Here’s What You Need To Know

If you're a homeowner planning to move, you're probably wondering what the process is going to look like and what you should tackle first:Is it better to start by finding your next home? Or should you sell your current house before you go out looking? Ultimately, what’s right for you depends on a lo

Read MoreShould You Buy a Vacation Home?

Some HighlightsNow that summer’s here, you may be planning your next getaway. But what if you didn’t have to? Buying a vacation home means having a built-in escape you can use year after year. It gives you the chance to generate rental income and have a go-to retirement destination in the future.If

Read MoreWhat You Should Know About Getting a Mortgage Today

If you’ve been putting off buying a home because you thought getting approved would be too hard, know this: qualifying for a mortgage is starting to get a bit more achievable, but lending standards are still strong.Lenders are making it slightly easier for well-qualified buyers to access financing,

Read MoreThink No One’s Buying Homes Right Now? Think Again.

If you’ve seen headlines saying home sales are down compared to last year, you might be thinking – is it even a good time to sell? Here’s the thing. Sure, the pace of the market has cooled compared to the frenzy we saw just a few years ago, but that’s not a red flag. It’s a return to normal. And nor

Read MoreWhy Big Investors Aren’t a Challenge for Today’s Homebuyer

Remember the chatter in the headlines about all the homes big institutional investors were buying? If you were thinking about buying a home yourself, you may have wondered how you’d ever be able to compete with that. Here’s the thing. That’s not the challenge so many people think it is – especially

Read MoreMulti-Generational Homebuying Hit a Record High – Here’s Why

Multi-generational living is on the rise. According to the National Association of Realtors (NAR), 17% of homebuyers purchase a home to share with parents, adult children, or extended family. That’s the highest share ever recorded by NAR (see graph below): And what’s behind the increase? Affordabili

Read MoreThink It’s Better To Wait for a Recession Before You Move? Think Again.

Fear of a recession is back in the headlines. And if you’re thinking about buying or selling sometime soon, that may leave you wondering if you should reconsider the timing of your move. A recent survey by John Burns Research and Consulting (JBREC) and Keeping Current Matters (KCM) shows 68% of peop

Read MoreWhy Homeownership Is Going To Be Worth It

Life can feel a bit unpredictable these days. What’s happening with inflation? The economy? The housing market? But in the middle of all that uncertainty, there’s one thing a lot of people still crave – a place to call their own. Because when everything else feels up in the air, home can be the thin

Read More3 Reasons To Buy a Home This Summer

Are you thinking about buying a home, but not sure if now’s the right time? A lot of people are waiting and wondering what the market’s going to do next. But here’s something only the savviest buyers realize: This summer might actually be the best time to buy in years. Here are three big reasons why

Read MoreIs Inventory Getting Back To Normal?

After years of it feeling almost impossible to find a home you want to buy, things are changing for the better. Nationally, inventory is growing, and that gives you more options for your move. But here’s what you need to know. That level of growth is going to vary based on where you live. And that’s

Read MoreBuying Your First Home? FHA Loans Can Help

If you’re a first-time homebuyer, you might feel like the odds are stacked against you in today’s market. But there are resources and programs out there that can help – if you know where to look. And one thing that can make homeownership easier to achieve? An FHA home loan. They’re designed to help

Read MoreThe Big Difference Between a Homeowner’s and a Renter’s Net Worth

Some HighlightsHomeownership is one of the best ways to build wealth in our country and it’s easy to see why.As you pay down your mortgage and as home values rise over time, you gain equity – and that helps grow your net worth. That’s why a homeowner’s net worth is nearly 40X greater than a renters.

Read More

Categories

Recent Posts