Are More Homeowners Selling as Mortgage Rates Come Down?

If you’re looking to buy a home, the recent downward trend in mortgage rates is good news because it helps with affordability. But there’s another way this benefits you – it may inspire more homeowners to put their houses up for sale. The Mortgage Rate Lock-In Effect Over the past year, one factor t

Read MoreExperts Project Home Prices Will Increase in 2024

Even though home prices are going up nationally, some people are still worried they might come down. In fact, a recent survey from Fannie Mae found that 24% of people think home prices will actually decline over the next 12 months. That means almost one out of every four people are dealing with that

Read MoreKey Terms Every Homebuyer Should Learn

3 Key Factors Affecting Home Affordability

Over the past year, a lot of people have been talking about housing affordability and how tight it’s gotten. But just recently, there’s been a little bit of relief on that front. Mortgage rates have gone down since their most recent peak in October. But there’s more to being able to afford a home th

Read MoreHomeownership Is Still at the Heart of the American Dream

Buying a home is a powerful decision, and it remains at the heart of the American Dream. Unlike renting, owning a home means more than just having a place to live – it offers a sense of belonging, stability, and freedom. According to Nicole Bachaud, Senior Economist at Zillow: “The American Dream is

Read MoreThe Dramatic Impact of Homeownership on Net Worth

If you're trying to decide whether to rent or buy a home this year, here's a powerful insight that could give you the clarity and confidence you need to make your decision. Every three years, the Federal Reserve releases the Survey of Consumer Finances (SCF), which compares net worth for homeowners

Read MoreAvoid These Common Mistakes After Applying for a Mortgage

If you’re getting ready to buy a home, it’s exciting to jump a few steps ahead and think about moving in and making it your own. But before you get too far down the emotional path, there are some key things to keep in mind after you apply for your mortgage and before you close. Here’s a list of thin

Read MoreWays Your Home Equity Can Help You Reach Your Goals

If you’ve owned your house for at least a couple of years, there’s something you’re going to want to know more about – and that’s home equity. If you’re not familiar with that term, Freddie Mac defines it like this: “. . . your home’s equity is the difference between how much your home is worth and

Read MoreWhat Lower Mortgage Rates Mean for Your Purchasing Power

If you want to buy a home, it's important to know how mortgage rates impact what you can afford and how much you’ll pay each month. Fortunately, rates for 30-year fixed mortgages have come down significantly since the end of October and are currently under 7%, according to Freddie Mac (see graph bel

Read MoreAchieving Your Homebuying Dreams in 2024

Some HighlightsPlanning to buy a home in 2024? Here’s what to focus on.Improve your credit score, plan for your down payment, get pre-approved, and decide what’s most important to you.Partner with a trusted real estate agent so you have expert advice on how to achieve your homebuying goals this year

Read MoreWhy Pre-Approval Is Your Homebuying Game Changer

If you’re thinking about buying a home, pre-approval is a crucial part of the process you definitely don’t want to skip. So, before you start picturing yourself in your new living room or dining on your future all-season patio, be sure you’re working with a trusted lender to prioritize this essentia

Read MoreThinking About Buying a Home? Ask Yourself These Questions

If you’re thinking of buying a home this year, you’re probably paying closer attention than normal to the housing market. And you’re getting your information from a variety of channels: the news, social media, your real estate agent, conversations with friends and loved ones, the list goes on and on

Read More3 Keys To Hitting Your Homeownership Goals in 2024

If buying or selling a home is your goal for 2024, it’s important to understand today’s housing market, know your why, and work with industry experts to bring your homeownership vision for the new year into focus. Over the last year, the economy had a big impact on the housing market, and likely on

Read MoreWhat You Need To Know About Saving for a Home in 2024

If you’re planning to buy a home, knowing what to budget for and how to save may sound intimidating – but it doesn’t have to be. One way to ease those concerns is to make sure you understand some of the costs you may encounter up front. And to do that, always turn to trusted real estate professional

Read MoreGet Ready To Buy a Home by Improving Your Credit Score

As the new year approaches, the idea of buying a home might be on your mind. It’s an exciting goal to set, and it's never too early to start laying the groundwork. One crucial step to prepare for homeownership is building a solid credit score. Lenders review your credit to assess your ability to mak

Read MoreExpert Quotes on the 2024 Housing Market Forecast

If you’re thinking about buying or selling a home soon, you probably want to know what you can expect from the housing market in 2024. In 2023, higher mortgage rates, confusion over home price headlines, and a lack of homes for sale created some challenges for buyers and sellers looking to make a mo

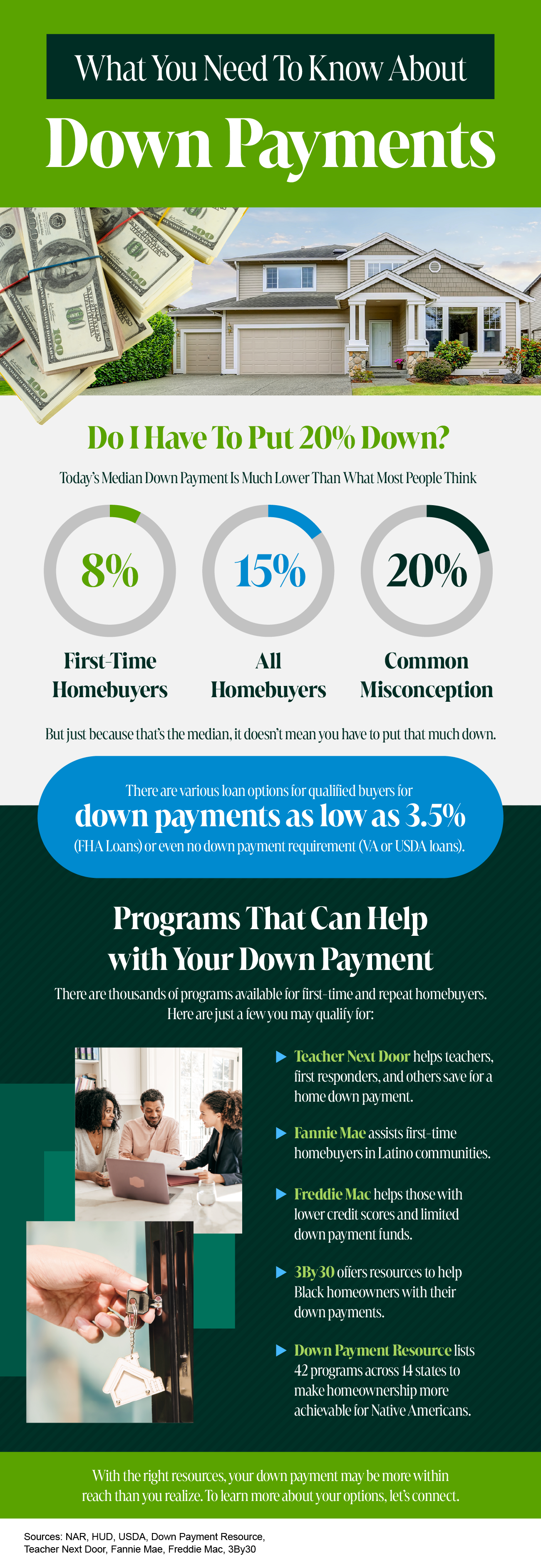

Read MoreWhat You Need To Know About Down Payments

The Surprising Trend in the Number of Homes Coming onto the Market

If you're thinking about moving, it's important to know what's happening in the housing market. Here's an update on the supply of homes currently for sale. Whether you're buying or selling, the number of homes in your area is something you should pay attention to. In the housing market, there are re

Read MoreDown Payment Assistance Programs Can Help Pave the Way to Homeownership

If you’re looking to buy a home, your down payment doesn’t have to be a big hurdle. According to the National Association of Realtors (NAR), 38% of first-time homebuyers find saving for a down payment the most challenging step. But the reality is, you probably don’t need to put down as much as you t

Read MoreThe Perfect Home Could Be the One You Perfect After Buying

There’s no denying mortgage rates and home prices are higher now than they were last year and that’s impacting what you can afford. At the same time, there are still fewer homes available for sale than the norm. These are two of the biggest hurdles buyers are facing today. But there are ways to over

Read More

Categories

Recent Posts