How Buying a Multi-Generational Home Helps with Affordability Today

In today's world of rising housing costs, many buyers are looking for ways to still be able to buy a home. Some of them have found a solution in multi-generational living. Multi-generational living is when two or more adult generations live together under one roof. This includes siblings, parents, o

Read MoreAre Higher Mortgage Rates Here To Stay?

Mortgage rates have been back on the rise recently and that’s getting a lot of attention from the press. If you’ve been following the headlines, you may have even seen rates recently reached their highest level in over two decades (see graph below): That can feel like a little bit of a gut punch

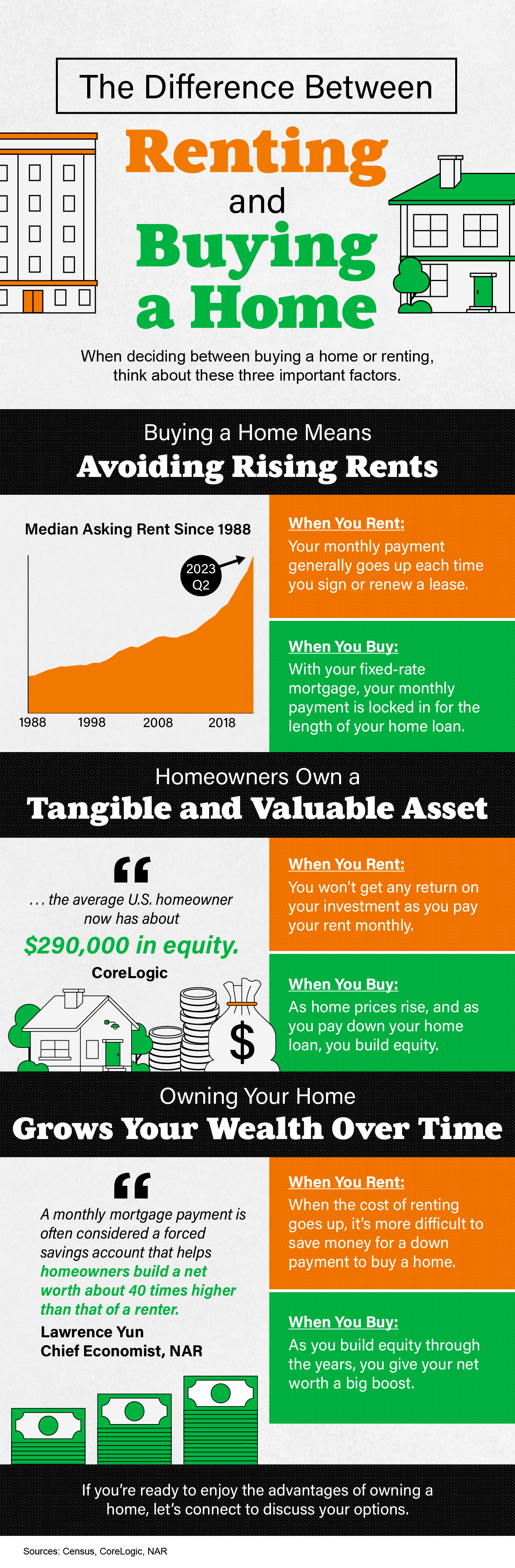

Read MoreThe Difference Between Renting and Buying a Home

Growing Your Net Worth with Homeownership

Take a moment to imagine where you want to be in a few years. You might be thinking about your job, money, wanting more stability, or goals you want to reach soon. Is homeownership a part of that vision? If it is, you should know owning a home has a whole lot of financial benefits. One of the many r

Read MoreThe Latest Expert Forecasts for Home Prices in 2023

Are you thinking about making a move? If so, all the speculation that home prices would crash this year may have you feeling a bit on edge about your decision. Let the data and the experts reassure you. Prices aren’t in a downward spiral and will actually finish the year strong. Even though you may

Read MoreAre Grandparents Moving To Be Closer to Their Grandkids?

During the pandemic, many people distanced themselves from their loved ones for health reasons. Grandparents were told to stay away from their grandkids, especially as schools started to open. That’s because it would have been risky to visit with their grandchildren who may have gotten sick from sch

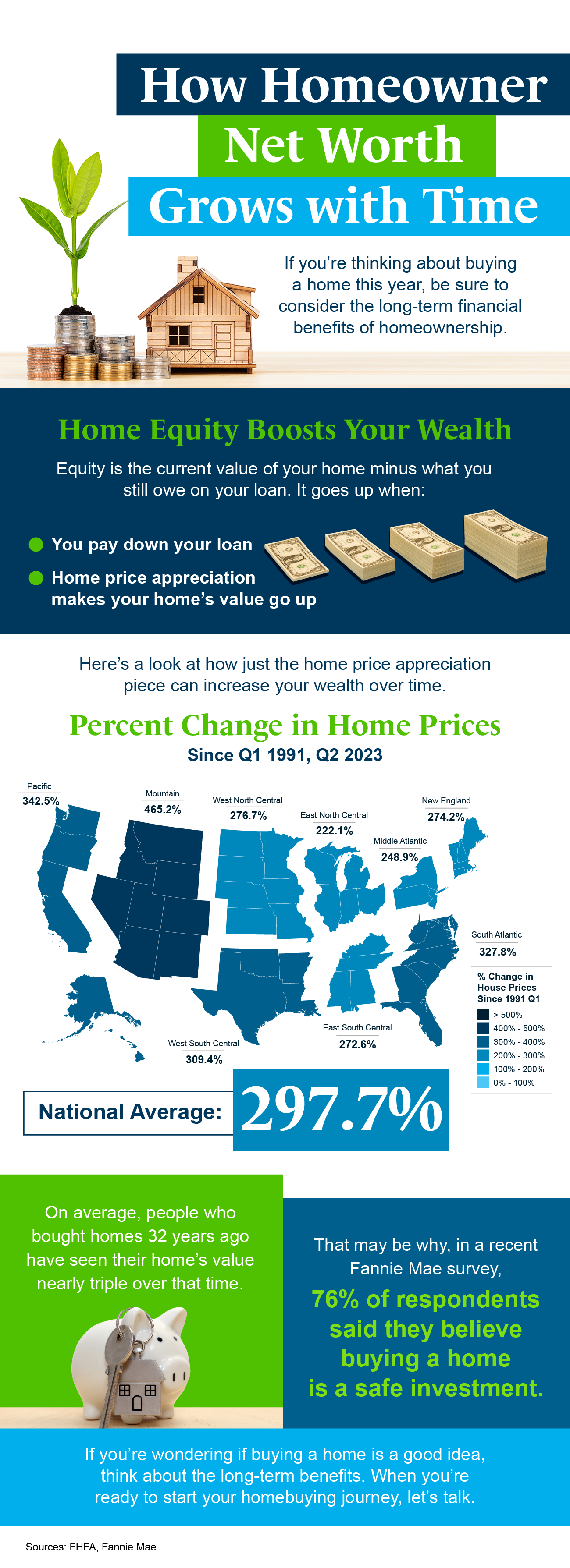

Read MoreHow Homeowner Net Worth Grows with Time

Are You a Homebuyer Worried About Climate Risks?

The increasing effects of natural disasters are leading to new obstacles in residential real estate. As a recent article from CoreLogic explains: “As the specter of climate change looms large, the world braces for unprecedented challenges. In the world of real estate, one of those challenges will b

Read MoreUnderstanding the Benefits of Owning Your First Home

Are you considering buying your first home? If so, it can be helpful to know what led other people to make that decision. According to a recent survey of first-time homebuyers by PulteGroup: “When asked why they purchased their first home recently, the answer was simple: because they wanted to. Eith

Read MoreUnpacking the Long-Term Benefits of Homeownership

If you’re thinking about buying a home soon, higher mortgage rates, rising home prices, and ongoing affordability concerns may make you wonder if it still makes sense to buy a home right now. While those market factors are important, there's more to consider. You should think about the long-term ben

Read MoreWhy Today’s Housing Inventory Shows a Crash Isn’t on the Horizon

You might remember the housing crash in 2008, even if you didn't own a home at the time. If you’re worried there’s going to be a repeat of what happened back then, there's good news – the housing market now is different from 2008. One important reason is there aren't enough homes for sale. That mean

Read MoreThe Return of Normal Seasonality for Home Price Appreciation

If you’re thinking of making a move, one of the biggest questions you have right now is probably: what’s happening with home prices? Despite what you may be hearing in the news, nationally, home prices aren’t falling. It’s just that price growth is beginning to normalize. Here’s the context you need

Read More-

If you’re looking to buy a home this fall, there are a few things you need to know. Affordability is tight with today’s mortgage rates and rising home prices. At the same time, there’s a limited number of homes on the market right now and that’s creating some competition among buyers. But, if you’re

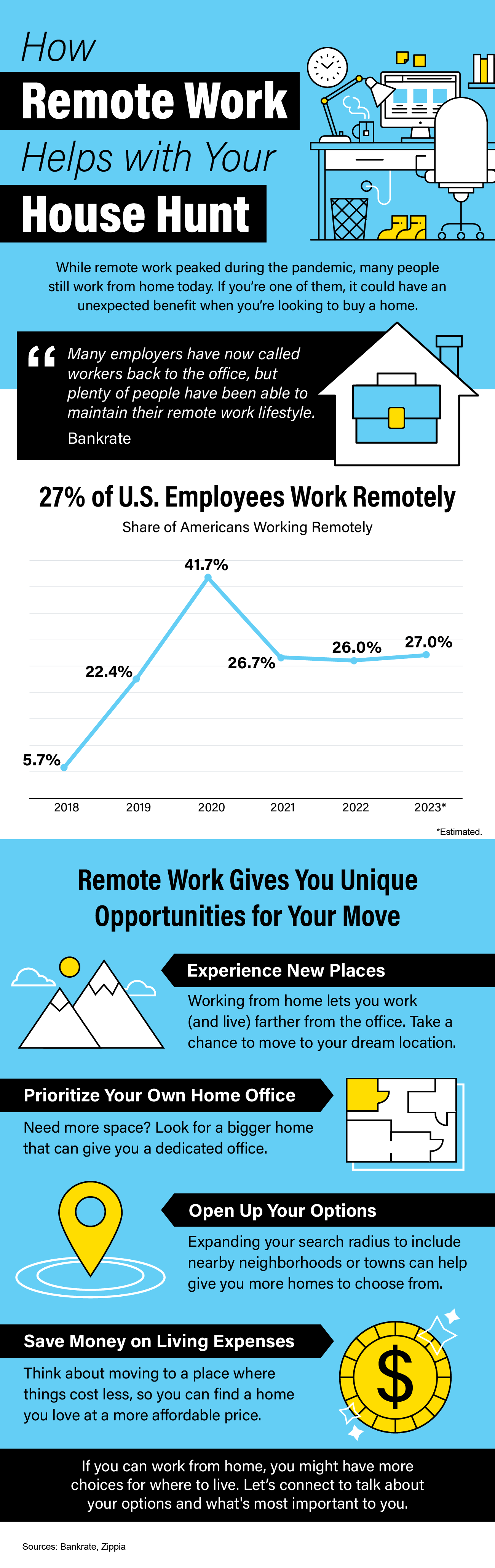

Read More How Remote Work Helps with Your House Hunt

The Many Non-Financial Benefits of Homeownership

Buying and owning your own home can have a big impact on your life. While there are financial reasons to become a homeowner, it's essential to think about the non-financial benefits that make a home more than just a place to live. Here are some of the top non-financial reasons to buy a home. Accordi

Read MoreRemote Work Is Changing How Some Buyers Search for Their Dream Homes

The way Americans work has changed in recent years, and remote work is at the forefront of this shift. Experts say it’ll continue to be popular for years to come and project that 36.2 million Americans will be working remotely by 2025. To give you some perspective, that's a 417% increase compared to

Read MoreWhy Is Housing Inventory So Low?

One question that’s top of mind if you’re thinking about making a move today is: Why is it so hard to find a house to buy? And while it may be tempting to wait it out until you have more options, that’s probably not the best strategy. Here’s why. There aren’t enough homes available for sale, but tha

Read MoreShould Baby Boomers Buy or Rent After Selling Their Houses?

Are you a baby boomer who’s lived in your current house for a long time and you’re ready for a change? If you’re thinking about selling your house, you have a lot to consider. Will you move to a different state or stay nearby? Is it time to downsize or do you want more space to accommodate your love

Read MoreWhat Experts Project for Home Prices Over the Next 5 Years

If you're planning to buy a home, one thing to consider is what experts project home prices will do in the future and how that might affect your investment. While you may have seen negative news over the past year about home prices, they’re doing far better than expected and are rising across the co

Read MoreGet Ready for Smaller, More Affordable Homes

Have you been trying to buy a home, but higher mortgage rates and home prices are limiting your options? If so, here’s some good news – based on what Ali Wolf, Chief Economist at Zonda, has to say – smaller, more affordable homes are on the way: “Buyers should expect that over the next 12 to 24 mont

Read More

Categories

Recent Posts