How Inflation Affects the Housing Market

Have you ever wondered how inflation impacts the housing market? Believe it or not, they’re connected. Whenever there are changes to one, both are affected. Here’s a high-level overview of the connection between the two. The Relationship Between Housing Inflation and Overall Inflation Shelter inflat

Read MoreGen Z: The Next Generation Is Making Moves in the Housing Market

Generation Z (Gen Z) is eager to put down their own roots and achieve financial independence. As a result, they’re turning to homeownership. According to the latest Home Buyers and Sellers Generational Trends Report from the National Association of Realtors (NAR), 30% of Gen Z buyers transitioned st

Read MoreWhy You Need a True Expert in Today’s Housing Market

The housing market continues to shift and change, and in a fast-moving landscape like we’re in right now, it’s more important than ever to have a trusted real estate agent on your side. Whether you’re buying your first home or selling once again, it’s mission critical to work with an expert who can

Read MoreWhy You Don’t Need To Fear the Return of Adjustable-Rate Mortgages

If you remember the housing crash back in 2008, you may recall just how popular adjustable-rate mortgages (ARMs) were back then. And after years of being virtually nonexistent, more people are once again using ARMs when buying a home. Let’s break down why that’s happening and why this isn’t cause fo

Read MoreWhy Median Home Sales Price Is Confusing Right Now

The National Association of Realtors (NAR) is set to release its most recent Existing Home Sales (EHS) report tomorrow. This monthly release provides information on the volume of sales and price trends for homes that have previously been owned. In the upcoming release, it’ll likely say home prices a

Read MorePeople Want Less Expensive Homes – And Builders Are Responding

In today’s housing market, there are two main affordability challenges impacting buyers: mortgage rates that are higher than they’ve been the past couple of years, and rising home prices caused by low inventory. To overcome those challenges, many people are working with their agents to find less exp

Read MoreDon’t Expect a Flood of Foreclosures

The rising cost of just about everything from groceries to gas right now is leading to speculation that more people won’t be able to afford their mortgage payments. And that’s creating concern that a lot of foreclosures are on the horizon. While it’s true that foreclosure filings have gone up a bit

Read MoreWhere Are People Moving Today and Why?

Plenty of people are still moving these days. And if you’re thinking of making a move yourself, you may be considering the inventory and affordability challenges in the housing market and wondering what you can do to help offset those. A new report from Gravy Analytics provides insight into where pe

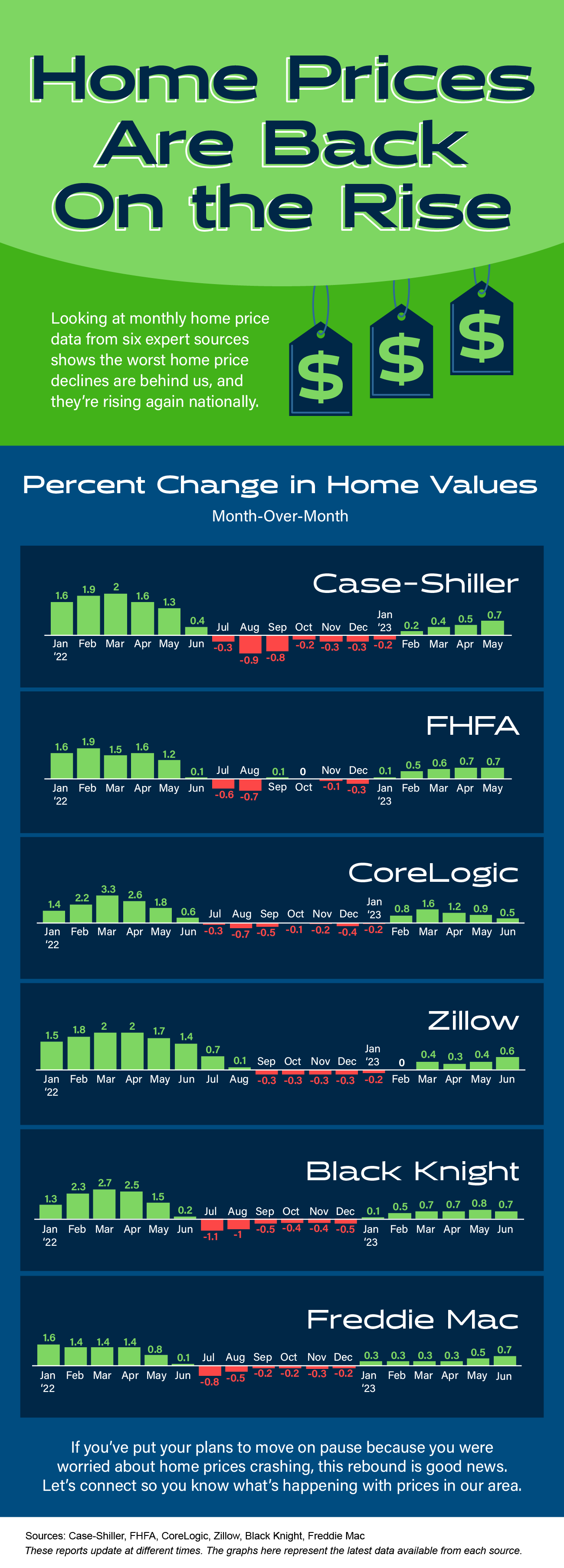

Read MoreHome Prices Are Back on the Rise

The Value of an Agent When Buying Your New Construction Home

Buying a new construction home can be an exciting experience. From being the very first owner, to customizing your home’s features, there are a lot of benefits. But navigating the complexities of buying a home that’s under construction can also be a bit overwhelming. This is where a skilled real est

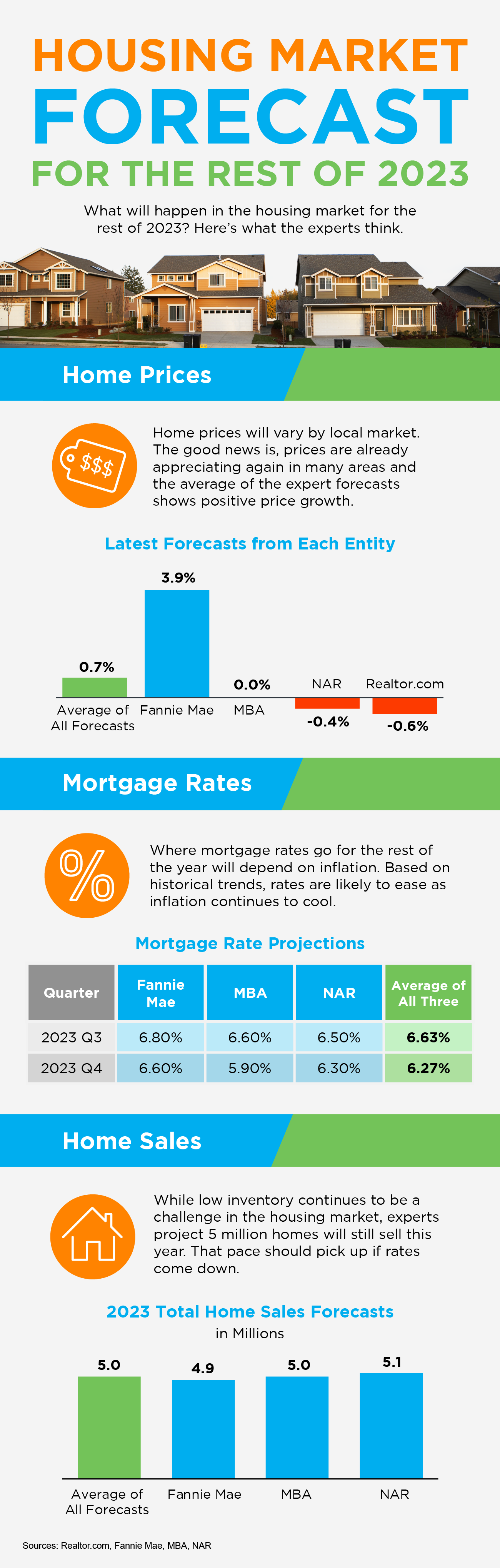

Read MoreHousing Market Forecast for the Rest of 2023

How Inflation Affects Mortgage Rates

When you read about the housing market in the news, you might see something about a recent decision made by the Federal Reserve (the Fed). But how does this decision affect you and your plans to buy a home? Here's what you need to know. The Fed is trying hard to reduce inflation. And even though the

Read MoreHow To Know If You’re Ready to Buy a Home

If you’re trying to decide if you’re ready to buy a home, there’s probably a lot on your mind. You’re thinking about your finances, today’s mortgage rates and home prices, the limited supply of homes for sale, and more. And, you’re juggling how all of those things will impact the choice you’ll make.

Read MoreTips for Making Your Best Offer on a Home

While the wild ride that was the ‘unicorn’ years of housing is behind us, today’s market is still competitive in many areas because the supply of homes for sale is still low. If you’re looking to buy a home this season, know that the peak frenzy of bidding wars is in the rearview mirror, but you may

Read MoreDon’t Fall for the Next Shocking Headlines About Home Prices

If you’re thinking of buying or selling a home, one of the biggest questions you have right now is probably: what’s happening with home prices? And it’s no surprise you don’t have the clarity you need on that topic. Part of the issue is how headlines are talking about prices. They’re basing their ne

Read MoreOwning Your Home Helps You Build Wealth

You may have heard some people say it’s better to rent than buy a home right now. But, even today, there are lots of good reasons to become a homeowner. One of them is that owning a home is typically viewed as a good long-term investment that helps your net worth grow over time. Homeownership Builds

Read MoreExplaining Today’s Mortgage Rates

If you’re following mortgage rates because you know they impact your borrowing costs, you may be wondering what the future holds for them. Unfortunately, there’s no easy way to answer that question because mortgage rates are notoriously hard to forecast. But, there’s one thing that’s historically

Read More-

If you’re following the news today, you may feel a bit unsure about what’s happening with home prices and fear whether or not the worst is yet to come. That’s because today’s headlines are painting an unnecessarily negative picture. If we take a year-over-year view, home prices did drop some, but th

Read More How Remote Work Expands Your Homebuying Horizons

Even as some companies transition back into the office, remote work remains a popular choice for many professionals. So, if you currently enjoy working from home or hope to be able to soon, you’re not alone. According to a recent survey, most working professionals want to work either fully remote or

Read MoreMomentum Is Building for New Home Construction

If you’re in the process of looking for a home today, you know the supply of homes for sale is low because you’re feeling the impact of having a limited pool of options. And, if your biggest hurdle right now is that you’re having trouble finding something you like, don’t forget that a newly built ho

Read More

Categories

Recent Posts