The True Value of Homeownership

Buying and owning your home can make a big difference in your life by bringing you joy and a sense of belonging. And with June being National Homeownership Month, it’s the perfect time to think about all the benefits homeownership provides. Of course, there are financial reasons to buy a house, but

Read MoreKeys to Success for First-Time Homebuyers

Buying your first home is an exciting decision and a major milestone that has the power to change your life for the better. As a first-time homebuyer, it’s a vision you can bring to life, but, as the National Association of Realtors (NAR) shares, you’ll have to overcome some factors that have made i

Read MoreToday’s Real Estate Market: The ‘Unicorns’ Have Galloped Off

Comparing real estate metrics from one year to another can be challenging in a normal housing market. That’s due to possible variability in the market making the comparison less meaningful or accurate. Unpredictable events can have a significant impact on the circumstances and outcomes being compare

Read MoreOwning a Home Helps Protect Against Inflation

You’re probably feeling the impact of high inflation every day as prices have gone up on groceries, gas, and more. If you’re a renter, you’re likely experiencing it a lot as your rent continues to rise. Between all of those elevated costs and uncertainty about a potential recession, you may be wonde

Read MoreWhy Buying a Vacation Home Beats Renting One This Summer

For many of us, visiting the same vacation spot every year is a summer tradition that’s fun, relaxing, and restful. If that sounds like you, now’s the time to think about your plans and determine if buying a vacation home this year makes more sense than renting one again. According to Forbes: “. .

Read MoreWhy Buyers Need an Expert Agent by Their Side

The process of buying a home can feel a bit intimidating, even under normal circumstances. But today's market is still anything but normal. There continues to be a very limited number of homes for sale, and that’s creating bidding wars and driving home prices back up as buyers compete over the avail

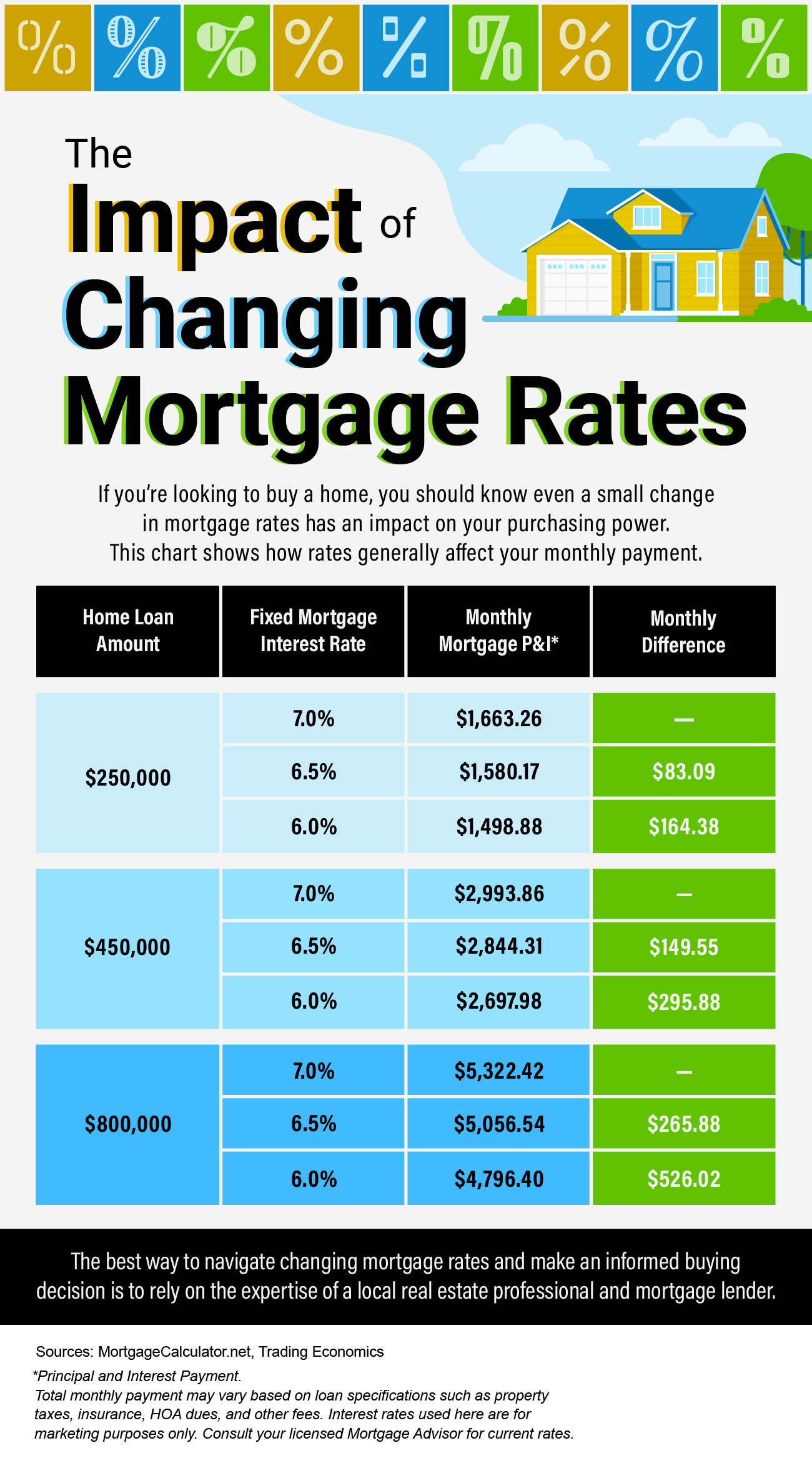

Read MoreThe Impact of Changing Mortgage Rates

What You Need To Know About Home Price News

The National Association of Realtors (NAR) will release its latest Existing Home Sales Report tomorrow. The information it contains on home prices may cause some confusion and could even generate some troubling headlines. This all stems from the fact that NAR will report the median sales price, whil

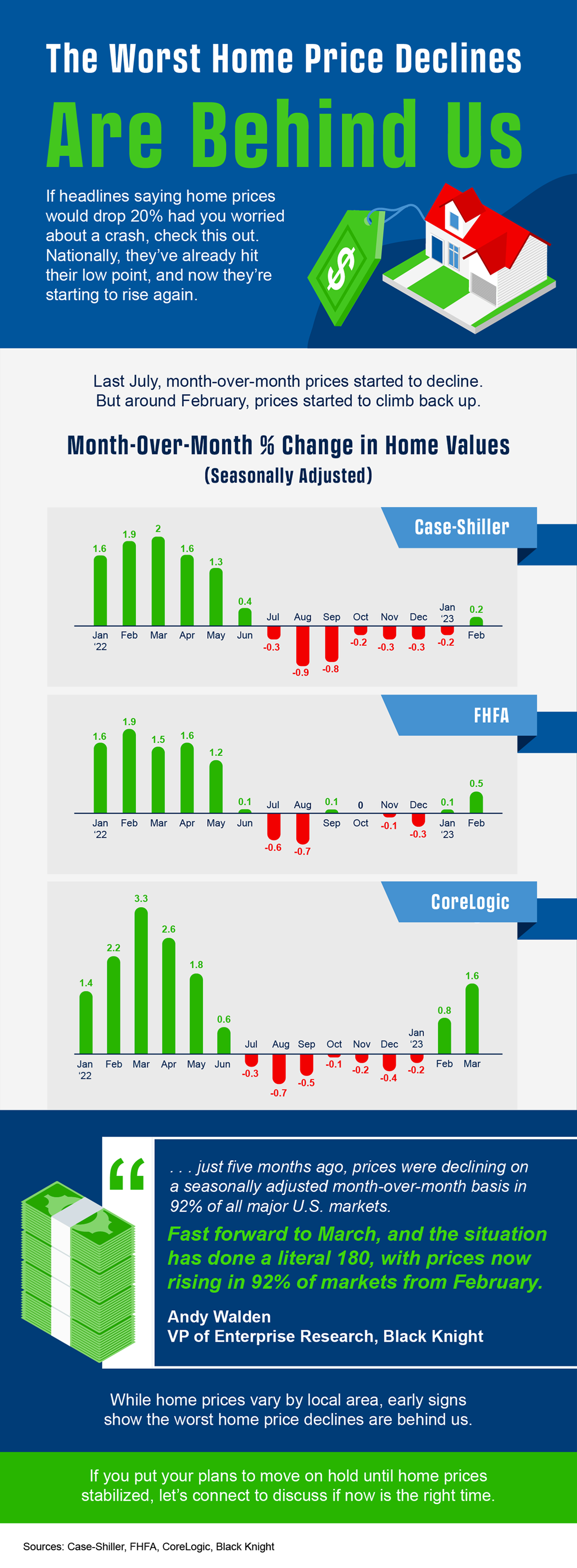

Read MoreThe Worst Home Price Declines Are Behind Us

If you’re following the news today, you may feel a bit unsure about what’s happening with home prices and fear whether or not the worst is yet to come. That’s because today’s headlines are painting an unnecessarily negative picture. Contrary to those headlines, home prices aren’t in a freefall. The

Read MoreHomeowners Have Incredible Equity To Leverage Right Now

Even though home prices have moderated over the last year, many homeowners still have an incredible amount of equity. But what is equity? In the simplest terms, equity is the difference between the market value of your home and the amount you owe on your mortgage. The National Association of Realtor

Read MoreThe Worst Home Price Declines Are Behind Us

Why Today’s Housing Market Is Not About To Crash

There’s been some concern lately that the housing market is headed for a crash. And given some of the affordability challenges in the housing market, along with a lot of recession talk in the media, it’s easy enough to understand why that worry has come up. But the data clearly shows today’s market

Read MoreIt May Be Time To Consider a Newly Built Home

If you’re looking to buy a house, you may find today’s limited supply of homes available for sale challenging. When housing inventory is as low as it is right now, it can feel like a bit of an uphill battle to find the perfect home for you because there just isn’t that much to choose from. If you ne

Read MoreHow Homeowners Win When They Downsize

Downsizing has long been a popular option when homeowners reach retirement age. But there are plenty of other life changes that could make downsizing worthwhile. Homeowners who have experienced a change in their lives or no longer feel like their house fits their needs may benefit from downsizing to

Read MoreWhy Buying a Home Makes More Sense Than Renting Today

Wondering if you should continue renting or if you should buy a home this year? If so, consider this. Rental affordability is still a challenge and has been for years. That’s because, historically, rents trend up over time. Data from the Census shows rents have been climbing pretty steadily since 19

Read MoreWays To Overcome Affordability Challenges in Today’s Housing Market

Some Highlights With so few homes on the market right now, widening the scope of your search to include nearby areas could help you find more options in your budget. You can also work with a trusted lender to consider alternative financing options and search for down payment assistance. If you’ve be

Read MoreThe Three Factors Affecting Home Affordability Today

There’s been a lot of focus on higher mortgage rates and how they’re creating affordability challenges for today’s homebuyers. It’s true that rates climbed dramatically since the record-low we saw during the pandemic. But home affordability is based on more than just mortgage rates – it’s determined

Read More-

If you’re buying a home this spring, today’s housing market can feel like a challenge. With so few homes on the market right now, plus higher mortgage rates, it’s essential to have a firm grasp on your homebuying budget. You’ll also need a sense of determination to find the right house and act quick

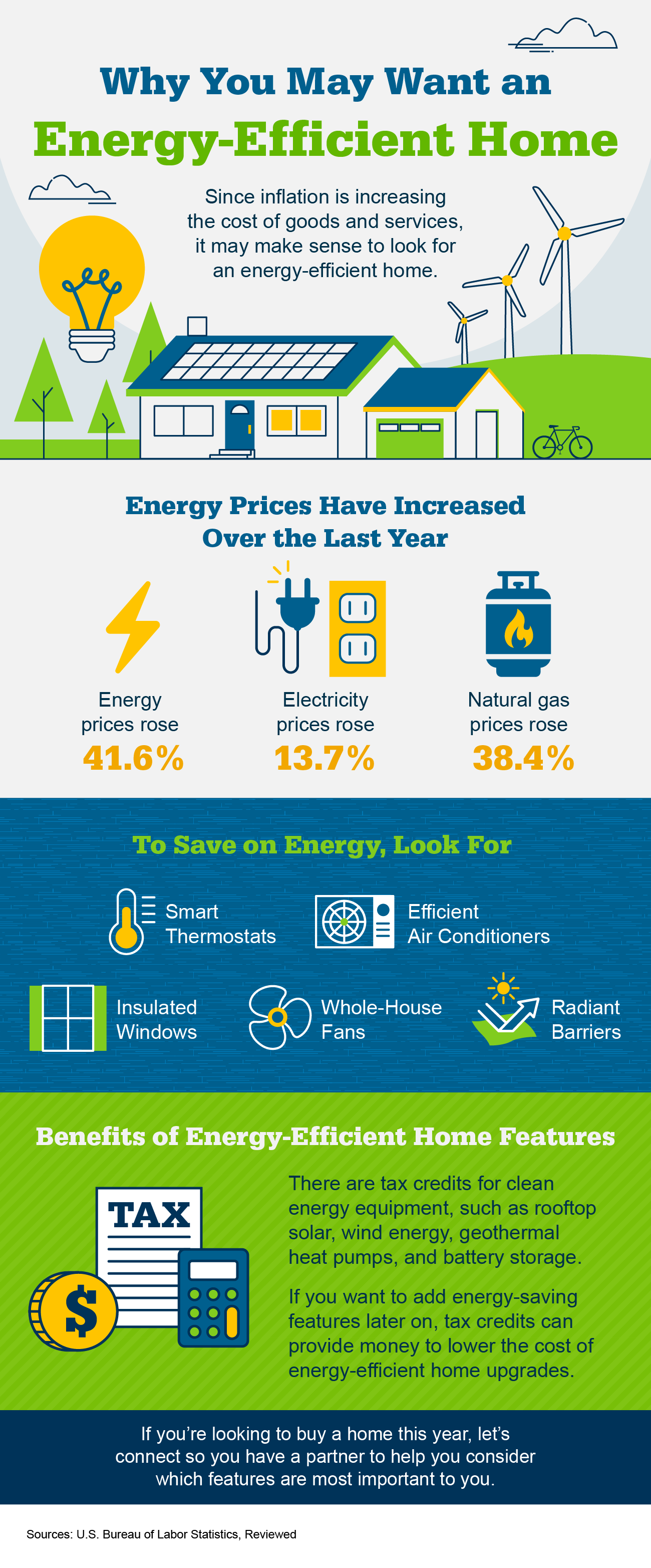

Read More Why You May Want an Energy-Efficient Home

What’s the Difference Between a Home Inspection and an Appraisal?

If you’re planning to buy a home, an inspection is an important step in the process. It assesses the condition of the home before you finalize the transaction. It’s also a different step in the process from an appraisal, which is a professional evaluation of the market value of the home you’d like t

Read More

Categories

Recent Posts