5 Reasons Millennials Are Buying Homes

In the United States, there are over 72 million millennials. If you’re part of that generation and have thought about buying a home, you aren’t alone. According to Zonda, 98% of millennials want to become a homeowner at some point if they aren’t already. But why? There are plenty of reasons you may

Read MoreThink Twice Before Waiting for Lower Home Prices

As the housing market continues to change, you may be wondering where it’ll go from here. One factor you’re probably thinking about is home prices, which have come down a bit since they peaked last June. And you’ve likely heard something in the news or on social media about a price crash on the hori

Read MoreYour Tax Refund Can Help You Achieve Your Homebuying Goals

Have you been saving up to buy a home this year? If so, you know there are a variety of expenses involved – from your down payment to closing costs. But there’s good news – your tax refund can help you achieve your goals by paying for some of these expenses. SmartAsset estimates the average American

Read MoreThe Key Advantage of Investing in a Home

Trying To Buy a Home? Hang in There.

We’re still in a sellers’ market. And if you’re looking to buy a home, that means you’re likely facing some unique challenges, like difficulty finding a home and volatile mortgage rates. But keep in mind, there are some benefits to being a buyer in today’s market that give you good reason to stick w

Read MoreHow Changing Mortgage Rates Can Affect You

The 30-year fixed mortgage rate has been bouncing between 6% and 7% this year. If you’ve been on the fence about whether to buy a home or not, it’s helpful to know exactly how a 1%, or even a 0.5%, mortgage rate shift affects your purchasing power. The chart below helps show the general relationship

Read MoreHow Homeownership Is Life Changing for Many Women

How Homeownership Is Life Changing for Many Women Throughout Women’s History Month, we reflect on the impact women have in our lives, and that includes impact on the housing market. In fact, since at least 1981, single women have bought more homes than single men each year, and they make up 17% of a

Read MoreWhy Buying a Home Is a Sound Decision

If you’re thinking about buying a home, you want to know the decision will be a good one. And for many, that means thinking about what home prices are projected to do in the coming years and how that could impact your investment. This year, we aren’t seeing home prices fall dramatically. As the year

Read MoreReasons To Consider Condos in Your Home Search

Are you having trouble finding a home that fits your needs and your budget? If so, you should know there’s an option worth considering – condominiums, also known as condos. According to Bankrate: “A condo can be a more affordable entry point to homeownership than a single-family home. And as a homeo

Read MoreWhat’s Ahead for Home Prices in 2023

What’s Ahead for Home Prices in 2023 Over the past year, home prices have been a widely debated topic. Some have said we’ll see a massive drop in prices and that this could be a repeat of 2008 – which hasn’t happened. Others have forecasted a real estate market that could see slight appreciation or

Read MoreWhat Buyer Activity Tells Us About the Housing Market

What Buyer Activity Tells Us About the Housing Market Though the housing market is no longer experiencing the frenzy of a year ago, buyers are showing their interest in purchasing a home. According to U.S. News: “Housing markets have cooled slightly, but demand hasn’t disappeared, and in many places

Read MoreBalancing Your Wants and Needs as a Homebuyer This Spring

Though there are more homes for sale now than there were at this time last year, there’s still an undersupply with fewer houses available than in more normal, pre-pandemic years. The Monthly Housing Market Trends Report from realtor.com puts it this way: “While the number of homes for sale is incre

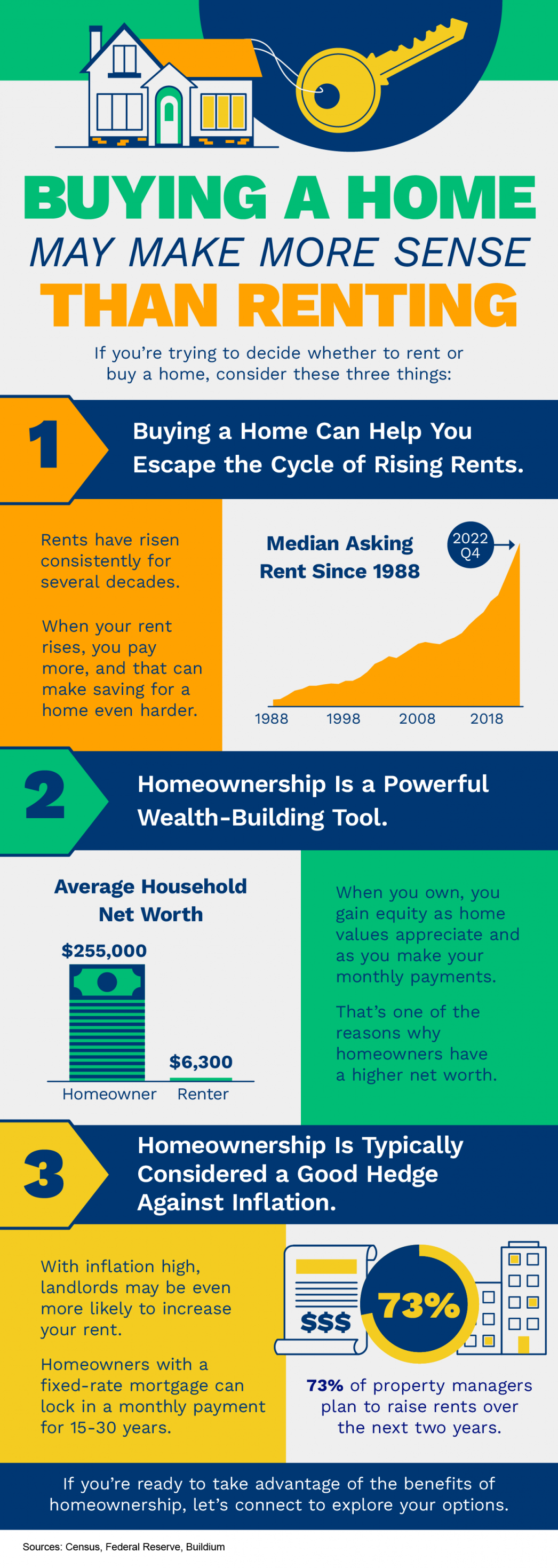

Read MoreBuying a Home May Make More Sense Than Renting

Buying a Home May Make More Sense Than Renting Some Highlights If you’re trying to decide whether to rent or buy a home, there are a few things you should consider. Homeownership can help you escape the cycle of rising rents, builds your wealth, and serves as a hedge against inflation. If you’re re

Read More4 Tips for Making Your Best Offer on a Home

4 Tips for Making Your Best Offer on a Home Are you planning to buy a home this spring? Though things are more balanced than they were at the height of the pandemic, it’s still a sellers’ market. So, when you find the home you want to buy, remember these four tips to make your best offer. 1.Lean on

Read MoreIs It Really Better To Rent Than To Own a Home Right Now?

Is It Really Better To Rent Than To Own a Home Right Now? You may have seen reports in the news recently saying it’s better to rent right now than it is to own your home. But before you let that impact your decisions, you should understand what these claims are based on. A lot of the time, these rep

Read MoreWhere Will You Go After You Sell Your House?

Where Will You Go After You Sell Your House? Some Highlights If you’re thinking of selling your house, be sure to explore all the options you have for your next home. Both newly built homes and existing homes offer plenty of unique benefits. If you have questions about the options in our area, let’

Read MoreWhat You Should Know About Rising Mortgage Rates

What You Should Know About Rising Mortgage Rates After steadily falling over the winter, mortgage rates have started to rise in recent weeks. This is concerning to some potential homebuyers as the combination of higher mortgage rates and higher prices have made homes less affordable. So, if you’re p

Read MoreOne Major Benefit of Investing in a Home

One Major Benefit of Investing in a Home One of the many reasons to buy a home is that it’s a major way to build wealth and gain financial stability. According to Freddie Mac: “Building equity through your monthly principal payments and appreciation is a critical part of homeownership that can help

Read MoreHow To Make Your Dream of Homeownership a Reality

How To Make Your Dream of Homeownership a Reality According to a recent Harris Poll survey, 8 in 10 Americans say buying a home is a priority, and 28 million Americans actually plan to buy within the next 12 months. Homeownership provides many financial and nonfinancial benefits, so that interest is

Read MoreA Smaller Home Could Be Your Best Option

A Smaller Home Could Be Your Best Option Many people are reaching the point in their lives when they need to decide where they want to live when they retire. If you’re a homeowner approaching this stage, you have several options to explore. Jessica Lautz, Deputy Chief Economist and Vice President of

Read More

Categories

Recent Posts