-

People Are Still Moving, Even with Today’s Affordability Challenges

If you're thinking about buying or selling a home, you might have heard that it’s tough right now because mortgage rates are higher than they’ve been over the past few years, and home prices are rising. That much is true. Take a look at the graph below. It breaks down how the current affordability s

Read MoreThe Latest 2024 Housing Market Forecast

The new year is right around the corner, and you might be wondering if 2024 will be the right time to buy or sell a home. If you want to make the most informed decision possible, it’s important to know what the experts have to say about what's ahead for the housing market. Spoiler alert: the project

Read MoreThese Top Cities Show Home Prices Are Still Climbing

If you’re considering buying a home or selling your current one to find something that better suits your needs, you may have questions about what’s happening with home prices today. Here’s what you need to know. There’s still a lot of confusion and misinformation out there. So, no matter what you ma

Read MoreLife-Changing Events That Move the Housing Market

Life is a journey filled with unexpected twists and turns, like the excitement of welcoming a new addition, retiring and starting a new adventure, or the bittersweet feeling of an empty nest. If something like this is changing in your own life, you may be considering buying or selling a house. That’

Read MoreVA Loans Help Heroes Achieve Homeownership

How VA Loans Can Help Make Homeownership Dreams Come True

For more than 79 years, Veterans Affairs (VA) home loans have helped millions of veterans buy their own homes. If you or someone you care about has served in the military, it's essential to learn about this program and its advantages. Here are some important things to know about VA loans before you

Read MoreThinking About Using Your 401(k) To Buy a Home?

Are you dreaming of buying your own home and wondering about how you’ll save for a down payment? You're not alone. Some people think about tapping into their 401(k) savings to make it happen. But before you decide to dip into your retirement to buy a home, be sure to consider all possible alternativ

Read MoreHomeowner Net Worth Has Skyrocketed

If you’re weighing your options to decide whether it makes more sense to rent or buy a home today, here’s one key data point that could help you feel more confident in making your decision. Every three years, the Federal Reserve Board releases the Survey of Consumer Finances (SCF). That report cover

Read MoreReasons To Sell Your House Before the New Year

As the year winds down, you may have decided it's time to make a move and put your house on the market. But should you sell now or wait until January? While it may be tempting to hold off until after the holidays, here are three reasons to make your move before the new year. Get One Step Ahead of Ot

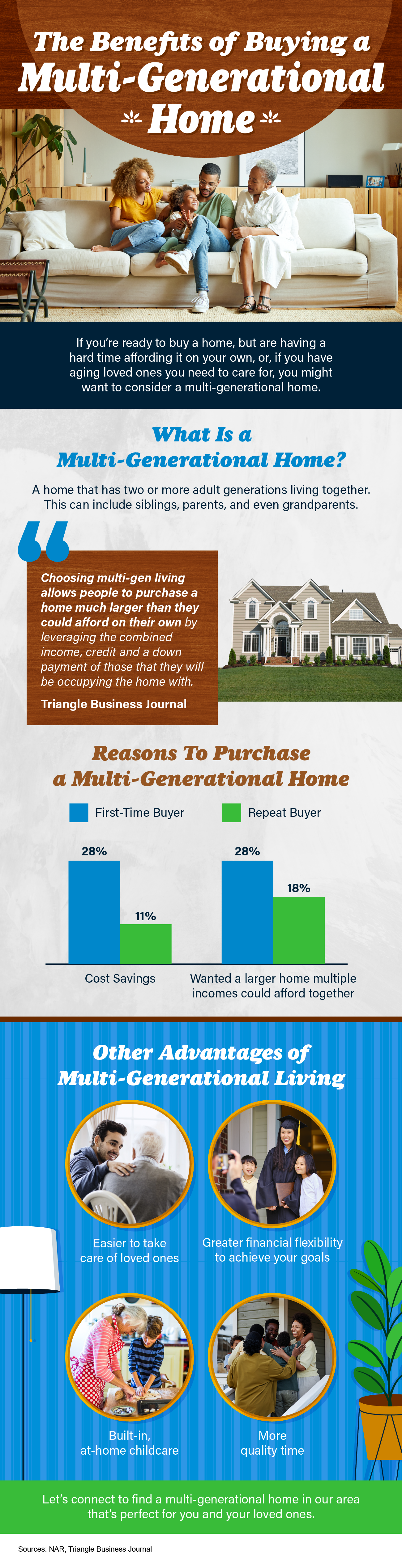

Read MoreThe Benefits of Buying a Multi-Generational Home

Don’t Believe Everything You Read About Home Prices

According to the latest data from Fannie Mae, 23% of Americans still think home prices will go down over the next twelve months. But why do roughly 1 in 4 people feel that way? It has a lot to do with all the negative talk about home prices over the past year. Since late 2022, the media has created

Read MoreWhat Are Accessory Dwelling Units and How Can They Benefit You?

Maybe you’re in the market for a home and are having a hard time finding the right one that fits your budget. Or perhaps you’re already a homeowner in need of extra income or a place for loved ones. Whether as a potential homebuyer or a homeowner with changing needs, accessory dwelling units, or ADU

Read MoreForeclosures and Bankruptcies Won’t Crash the Housing Market

If you've been following the news recently, you might have seen articles about an increase in foreclosures and bankruptcies. That could be making you feel uneasy, especially if you're thinking about buying or selling a house. But the truth is, even though the numbers are going up, the data shows the

Read MoreA Real Estate Agent Helps Take the Fear Out of the Market

Do negative headlines and talk on social media have you feeling worried about the housing market? Maybe you’ve even seen or heard something lately that scares you and makes you wonder if you should still buy or sell a home right now. Regrettably, when news in the media isn't easy to understand, it c

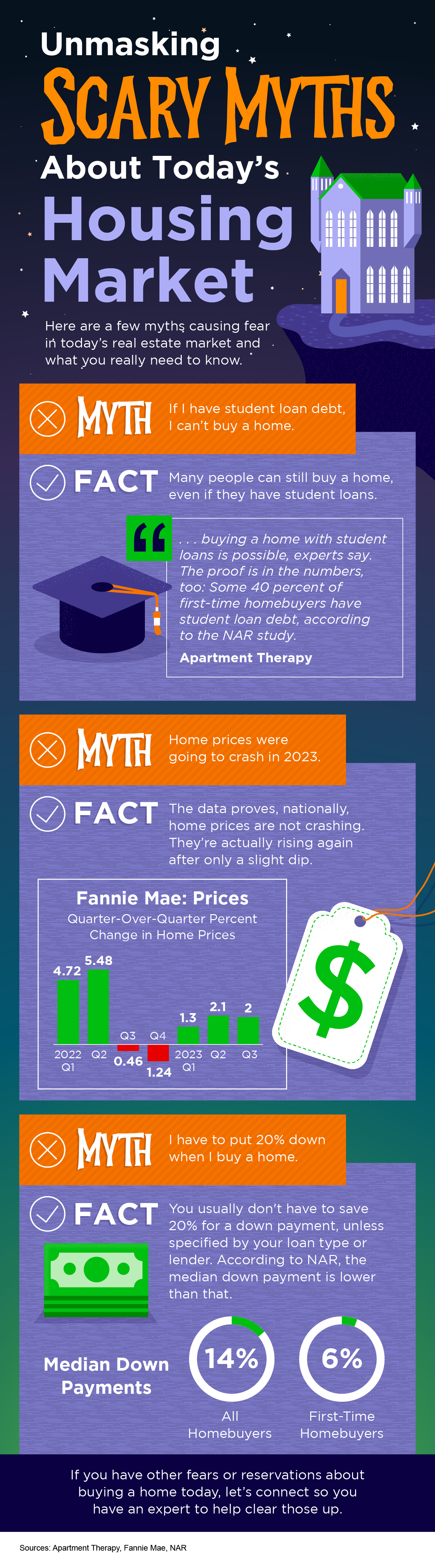

Read MoreUnmasking Scary Myths about Today’s Housing Market

Affordable Homeownership Strategies for Gen Z

The idea of owning a home has always been a big part of the American Dream. It's a symbol of stability, independence, and having a place to truly call your own. But for Gen Z, the "Zoomers" born between 1997 and 2012, making that dream a reality can feel like quite the challenge today with higher mo

Read MoreInvest in Yourself by Owning a Home

Are you wondering if it makes sense to buy a home right now? While today’s mortgage rates might seem a bit intimidating, here are two compelling reasons why it still may be a good time to become a homeowner. Home Values Appreciate over Time There’s been a lot of confusion around what’s happened with

Read MoreThe Perks of Selling Your House When Inventory Is Low

When it comes to selling your house, you’re probably trying to juggle the current market conditions and your own needs as you plan your move. One thing that may be working in your favor is how few homes there are for sale right now. Here’s what you need to know about the current inventory situation

Read More-

If you've ever dreamed of buying your own place, or selling your current house to upgrade, you're no stranger to the rollercoaster of emotions changing home prices can stir up. It's a tale of financial goals, doubts, and a dash of anxiety that many have been through. But if you put off moving becaus

Read More

Categories

Recent Posts